Invest with haatch

From Pre-Seed to exit

3 truths drive our investment strategy

Deep pain drives purchasing decisions, and the right solutions create sticky long-term recurring revenue.

Go-to-market and sales define a seed-stage company’s success, turning early traction into repeatable growth.

Hands-on operational experience from 0 to 1 is fundamental to guide founders through rapid scale.

Discover how the fund works and how to invest.

Request Here

%20%E2%80%93%20Growth%20Investor%20Awards.png)

We’ve been on the journey with over 150 companies.

“Haatch has progressed significantly in the past year and is now the best-established EIS manager of its age. Although the funds are five years old, the team has been investing for more than twice that, and brings a broad range of relevant knowledge. The early commitment from British Business Investments through the Regional Angels Programme is a notable endorsement for a newer manager.”

An introduction to Haatch

An Introduction to Haatch

Sourced and managed portfolios by ex-entrepreneurs with $200m+ exits.

Haatch Team

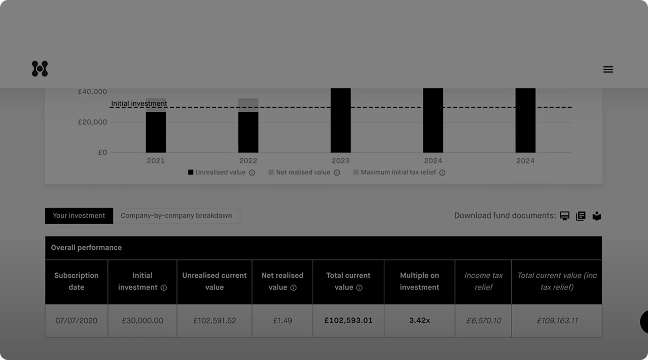

Haatch Investor Portal

Industry-leading investor relations with complete performance transparency.

Reuqest IM

Built by Operators, Proven by Results

£130m

7.4x

£52m

Resources

for Investors